As the 2026 filing season approaches, S corporations face an important tax deadline. The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, introduces significant tax updates that will impact S corporations when filing Form 1120-S for the 2025 tax year.

The OBBBA brings significant changes to tax provisions such as the Qualified Business Income (QBI) deduction, depreciation rules, and Section 179 expensing, all of which will influence how S corporations report their income, deductions, and credits. These updates could affect shareholder distributions and tax benefits, making it crucial for businesses to understand the changes.

Many S corporation owners are seeking clarity on how these updates affect their filings and how to ensure compliance with the new rules. In this guide, we’ll break down these changes and provide actionable steps to help S corporations file with confidence and optimize their tax outcomes.

What is Form 1120-S?

Form 1120-S is the U.S. Income Tax Return for an S Corporation, used by S corporations to report income, deductions, gains, losses, and credits to the IRS. An S corporation itself does not pay income taxes; instead, income, deductions, and credits pass through to the shareholders, who report them on their individual tax returns via Schedule K-1.

If you need further clarification, the IRS offers a comprehensive guide to help you understand the details of Form 1120-S.

Who needs to file Form 1120-S?

• S corporations that have elected S status under IRS rules are required to file Form 1120-S each year.

• LLCs taxed as S corporations must also file Form 1120-S.

It’s essential for S corporations to file this form accurately, as it impacts shareholder tax returns.

Key Filing Deadlines for 2026

Form 1120-S Filing Deadline: For calendar-year S corporations, the filing deadline for the 2025 tax year is March 15, 2026. Since March 15 falls on a weekend, the deadline is shifted to the next business day, March 16, 2026.

Extension Filing: S corporations can extend the deadline to September 15, 2026, by filing Form 7004.

Weekend or Holiday Adjustments: If the due date falls on a weekend or holiday, the deadline is extended to the next business day.

Filing Form 1120-S can be complex, but staying ahead of the deadline and ensuring all tax changes under the OBBBA are applied correctly will help you avoid penalties and optimize your tax outcomes. Filing early helps avoid last-minute issues, so it’s recommended to prepare ahead of time.

OBBBA Tax Changes Impacting S Corporations in 2026

The One Big Beautiful Bill Act (OBBBA), signed into law in 2025, brings significant tax changes for businesses, including S Corporations. The OBBBA aims to simplify tax laws and offer more benefits for businesses while addressing emerging economic trends. For S Corporations, these updates will affect how income, deductions, and certain credits are reported on Form 1120-S for the 2026 filing season.

Here are the key OBBBA changes that will impact S Corporations for the 2025 tax year:

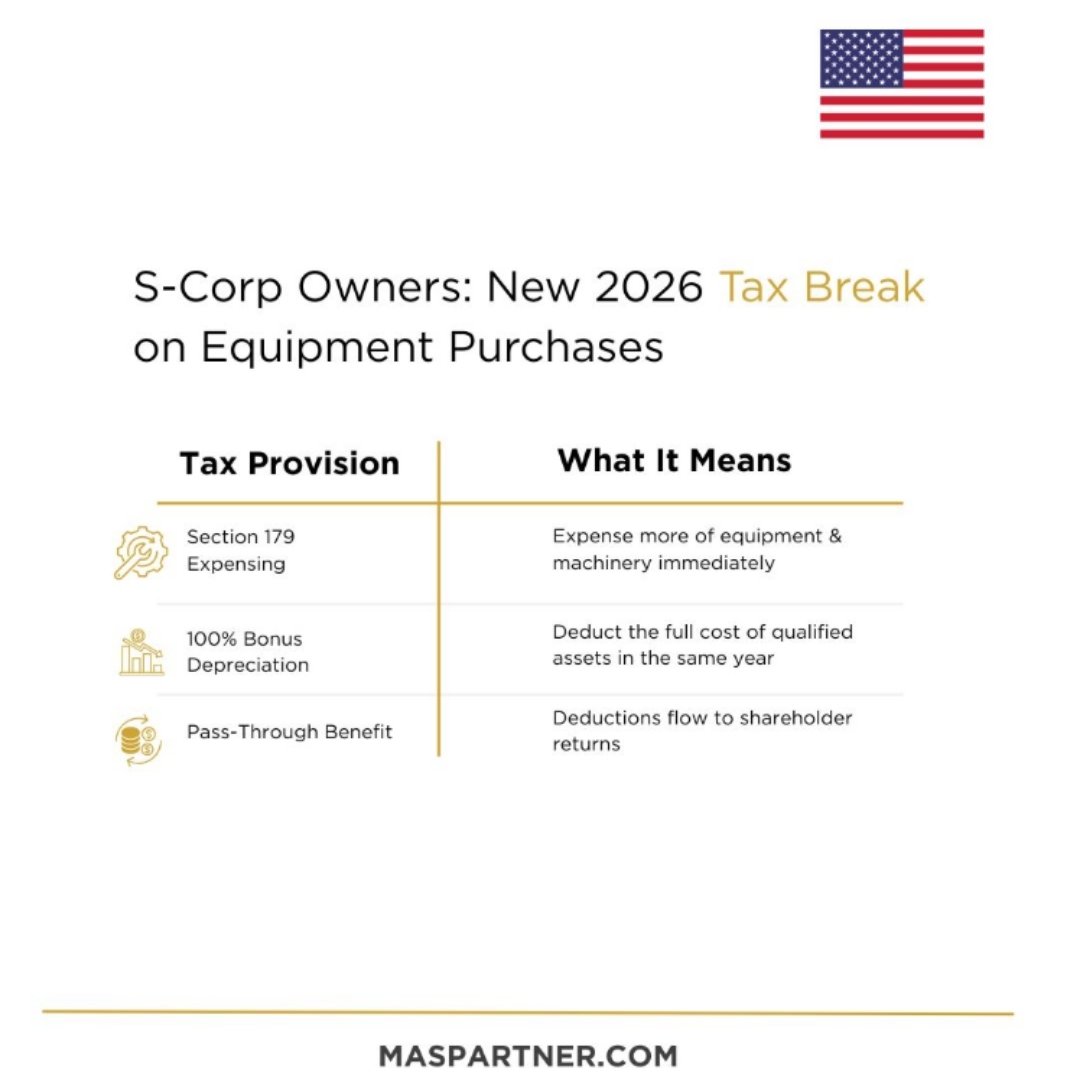

1. Enhanced Section 179 Expensing

The OBBBA increases the Section 179 expensing limit to $2,500,000 (up from $1,160,000 under prior law), with a phase-out beginning at $4,000,000 of total asset purchases, allowing S corporations toimmediately expense more of their capital investments in the year the assets are purchased.

Here’s how these changes break down:

• Immediate Expensing for Capital Purchases: S corporations can now expense larger purchases of machinery and equipment upfront instead of depreciating them over several years.

• Example: If an S corporation buys $500,000 in new equipment, it can expense a larger portion right away, reducing its taxable income.

Shareholders benefit from these immediate deductions, which flow through to their individual tax returns via Schedule K-1, potentially lowering their overall tax burden.

2. Bonus Depreciation Continuation

The OBBBA permanently restores 100% bonus depreciation for qualified property purchased and placed in service after January 19, 2025. This reverses the prior phase-down schedule (which had dropped to 60% in 2024) and makes full first-year expensing a permanent feature of the tax code.

Here’s how these changes break down:

• Full Deduction for Qualified Property: S corporations can fully deduct the cost of qualified assets, such as machinery or vehicles, in the year they are placed into service.

• Example: If an S corporation purchases $300,000 in new equipment, shareholders can claim a larger deduction on their 2025 tax year individual returns.

Shareholders benefit from these deductions, reducing their taxable income when the corporation makes large asset purchases.

3. QBI Deduction Extension

The QBI (Qualified Business Income) deduction under Section 199A is permanently extended and enhanced by the OBBBA, increasing the deduction from 20% to 23% of qualified business income on individual tax returns of S corporation shareholders.

Here’s how these changes break down:

• Increased Income Thresholds: The OBBBA raises the income thresholds for eligibility, enabling more S corporation shareholders to benefit from the QBI deduction.

• No Entity-Level Deduction: Although not deducted at the entity level, shareholders can continue to claim the deduction on their individual returns.

Shareholders should review their QBI eligibility and consult a tax professional to ensure they maximize the benefit, especially with the new enhanced thresholds applicable for the 2025 tax year.

4. Adjustments to S Corporation Distributions and Allocations

The OBBBA introduces greater scrutiny on how S corporations allocate income and make distributions to shareholders, requiring more detailed reporting.

Here’s how these changes break down:

• More Detailed Reporting: The IRS now mandates clearer reporting of distributions and allocations to ensure compliance with the new regulations.

• Impact on K-1: S corporations must ensure these transactions are accurately reflected in Schedule K-1.

Failure to report distributions and allocations correctly may lead to penalties or incorrect tax filings for shareholders.

5. Corporate Transparency Act (CTA) Reporting Requirements

The OBBBA revises Corporate Transparency Act (CTA) reporting rules by narrowing the range of entities required to submit beneficial ownership information. Rather than expanding requirements, the OBBBA limits beneficial ownership reporting to foreign-owned entities and U.S. companies with foreign ownership, effectively exempting most domestic S corporations from BOI filing obligations.

Here’s how these changes break down:

• New Reporting Requirements: Most domestic S corporations are now exempt from Beneficial Ownership Information (BOI) reporting. Only S corporations with 25% or more foreign ownership are required to file.

• Why it Matters: This relief is especially relevant for S corporations with all-domestic ownership, who are now fully exempt from BOI reporting under the OBBBA.

S corporations with any foreign ownership should verify their BOI filing obligations. Domestic-only S corporations should confirm they meet the exemption criteria and document their ownership structure accordingly.

Other Important Filing Considerations for S Corporations in 2026

1. Review Financial Statements: Ensure that QBI, Section 179, and bonus depreciation are correctly applied, and double-check capital investments, depreciation, and shareholder allocations to avoid errors.

2. Consult a Tax Professional: Receive expert guidance on navigating the latest tax updates under the OBBBA, including rules around R&E expense capitalization and corporate transparency requirements.

Common Mistakes to Avoid

1. Incorrect Allocation of Deductions and Distributions: Ensure that all income, deductions, and distributions are accurately reported on Schedule K-1 to avoid penalties or incorrect tax filings.

2. Misstated QBI deductions or R&E expenses: Carefully review Schedule K-1 to ensure accurate reporting and prevent problems for shareholder tax returns.

Conclusion

The One Big Beautiful Bill Act (OBBBA) brings important changes that will impact S corporations during the 2026 filing season, especially in areas like QBI deductions, bonus depreciation, and Section 179 expensing. Understanding and applying these updates correctly is essential for ensuring compliance and maximizing tax benefits.

By reviewing your financial statements, consulting with a tax professional, and avoiding common filing mistakes, S corporations can confidently navigate these changes, ensuring proper preparation and timely action to maximize tax benefits and set up their business for success in 2026 and beyond.

Book your free consultation today to ensure your S corporation is fully prepared for the 2026 filing season.

FAQs

1. What is the deadline for filing Form 1120-S in 2026?

For calendar-year S corporations, the deadline to file Form 1120-S for the 2025 tax year is March 16, 2026, since March 15 falls on a weekend. Businesses that require more time can request an extension by filing Form 7004, which extends the deadline to September 15, 2026.

2. What is Section 179expensingfor S corporations?

Section 179 allows S corporations to deduct the cost of qualifying equipment and machinery in the year it is purchased instead of depreciating it over several years. Under the OBBBA, the deduction limit increases to $2,500,000, enabling businesses to expense larger investments immediately.

3. Can S corporations claim 100% bonus depreciation?

Yes. The OBBBA permanently restores 100% bonus depreciation for qualified assets placed in service after January 19, 2025. This allows S corporations to deduct the full cost of eligible assets in the first year, reducing taxable income for shareholders.

4. How does the QBI deduction apply to S corporation owners?

The Qualified Business Income (QBI) deduction allows eligible S corporation shareholders to deduct a portion of their business income on their individual tax returns. Under the OBBBA, the deduction increases to 23% of qualified business income, subject to income limits and eligibility rules.

5. Do S corporations pay federal income tax?

No. S corporations are pass-through entities, meaning the corporation itself generally does not pay federal income tax. Instead, profits and losses are reported on Schedule K-1 and passed through to shareholders, who report them on their individual tax returns.